The Oil Production Contract (CPP), concerning the unified blocks of the Pande and Temane fields (on land), was concluded on 26 October 2000 between the Government of Mozambique, the National Hydrocarbon Company, E.P., Sasol Petroleum Temane Lda. and the Mozambican Hydrocarbon Company, SARL. to produce and market natural and condensed gas in markets in Mozambique and South Africa.

The gas produced from these fields is processed at the Natural Gas Processing Center (CPF) in Temane and transported by a pipeline (Mozambique to Seconda Pipeline-MSP) of about 867 km of extension, for supply in the national and South African market.

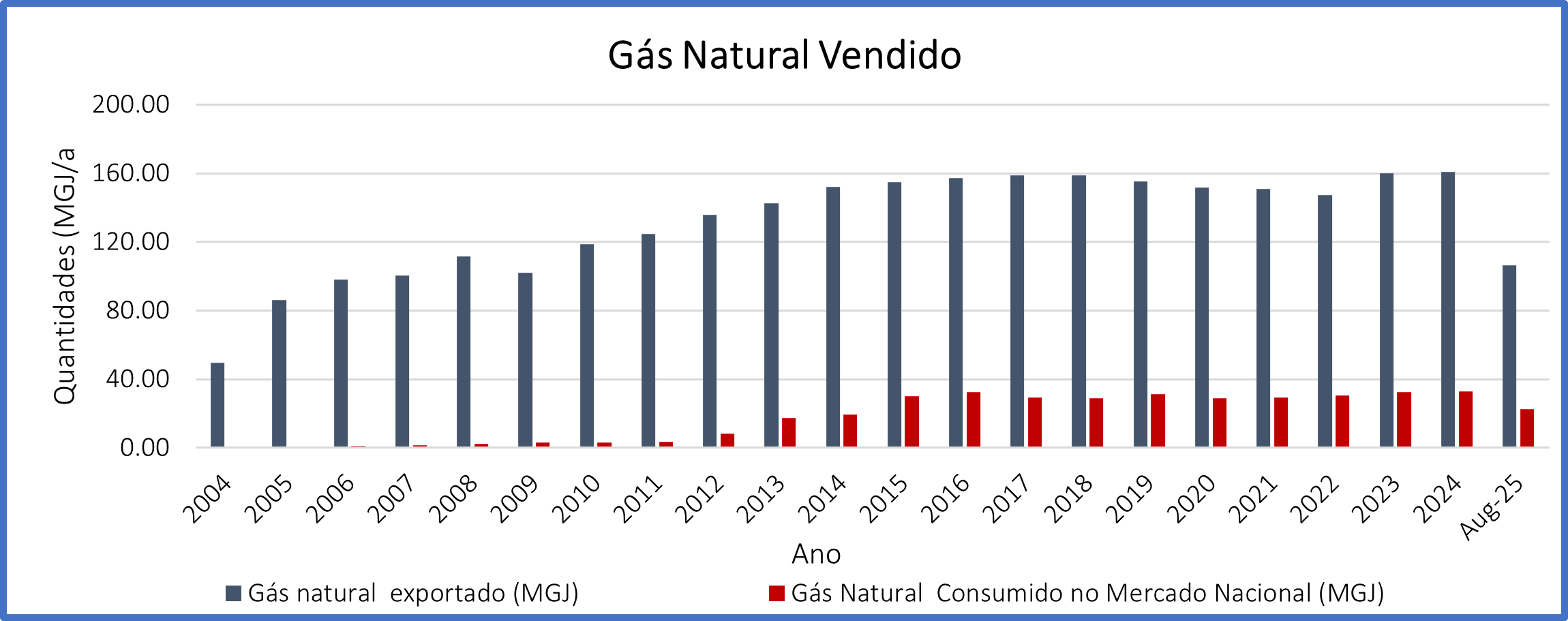

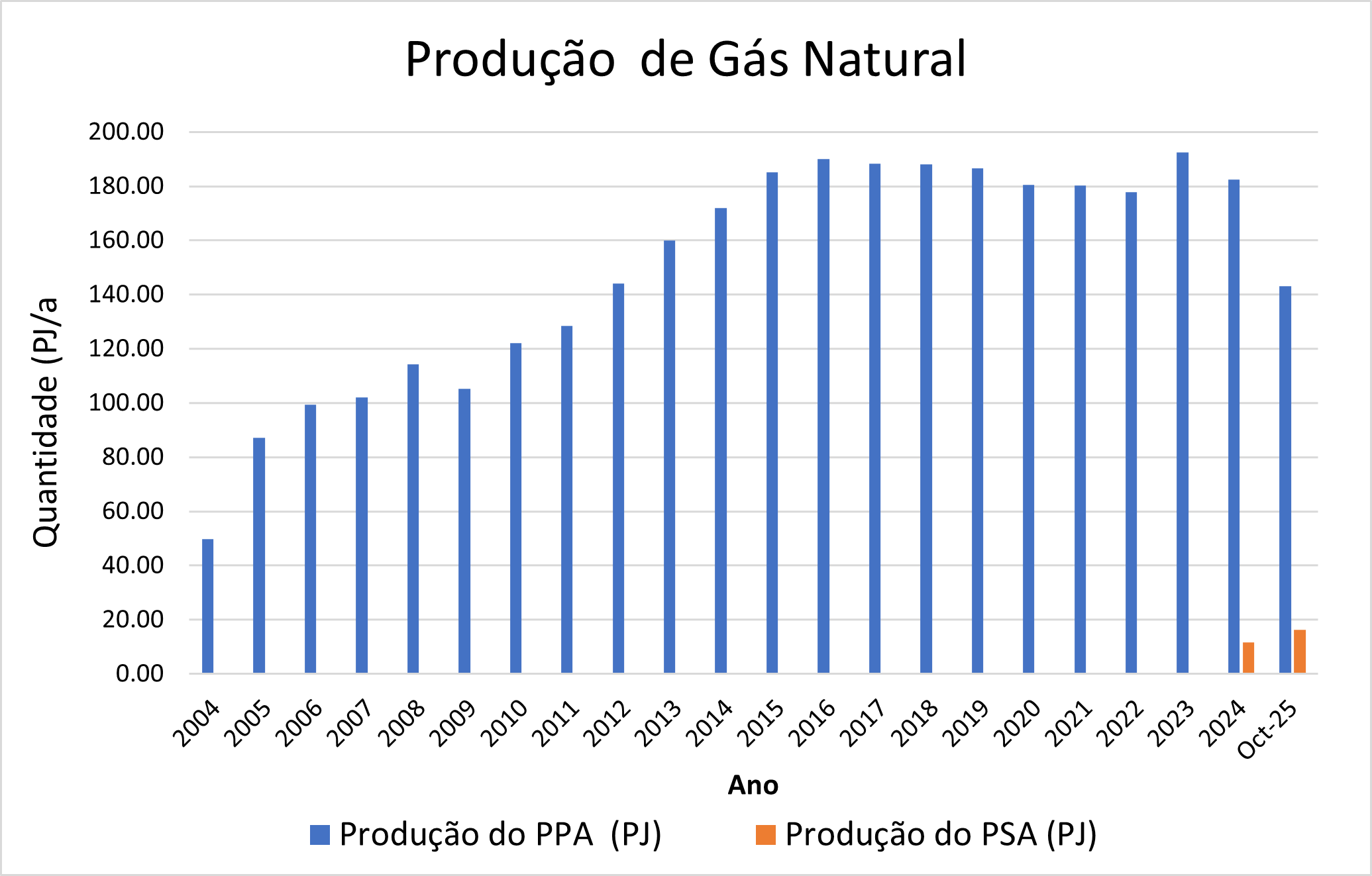

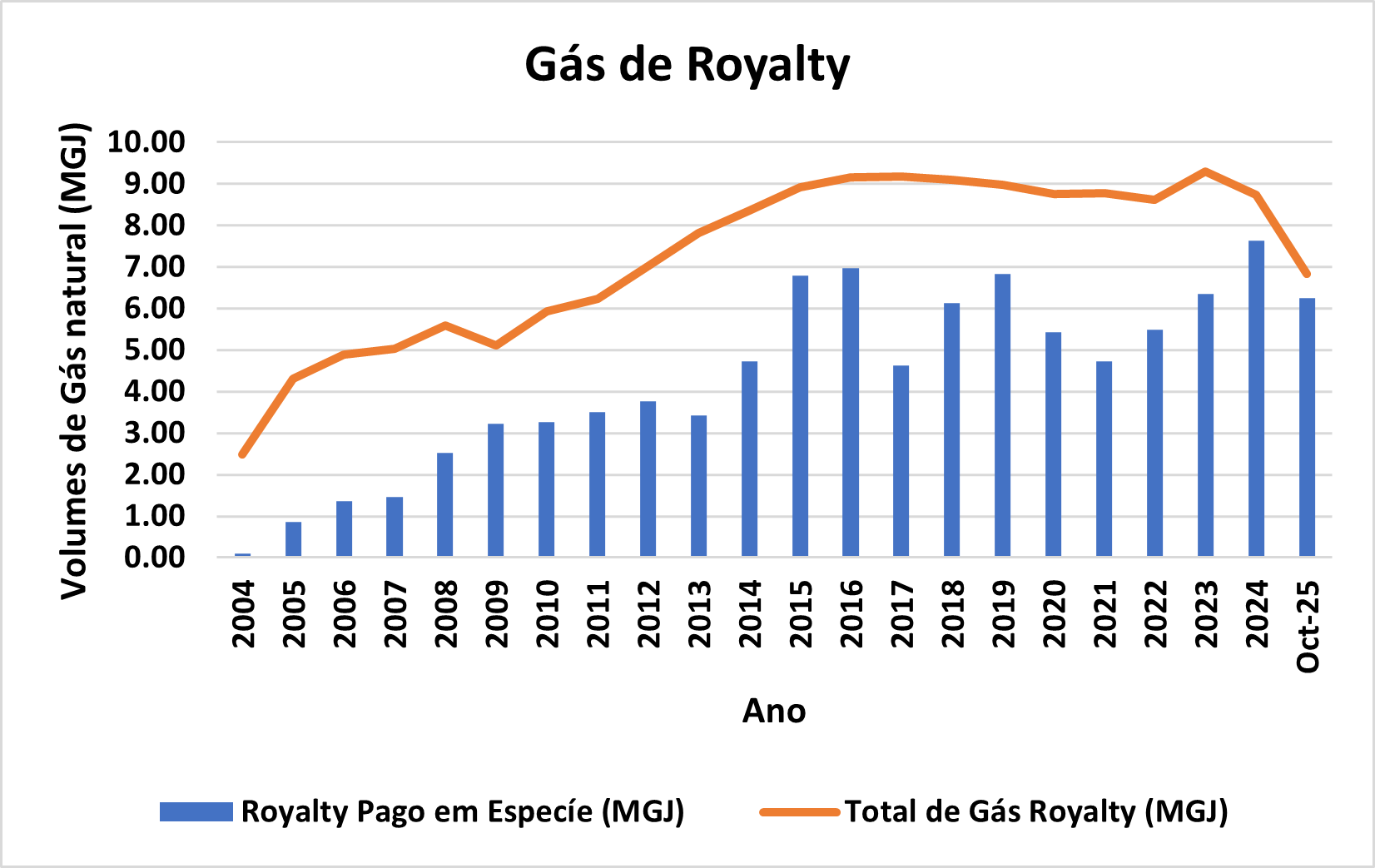

Natural gas production began in 2004, with a contract capacity of 120 Million Giga Joules/year (MGJ/a) through the First Gas Sale Contract (GSA1), and which suffered successive expansions until reaching the current contract capacity of 197 MGJ/a, accommodating the contractual obligations of the first, second and third gas sales contract (GSA1, GSA2 and GSA 3) including the IPP;

The IPP due to the Government under the APP corresponds to 5% of gas produced and sold and may be delivered in kind or in monetary value.

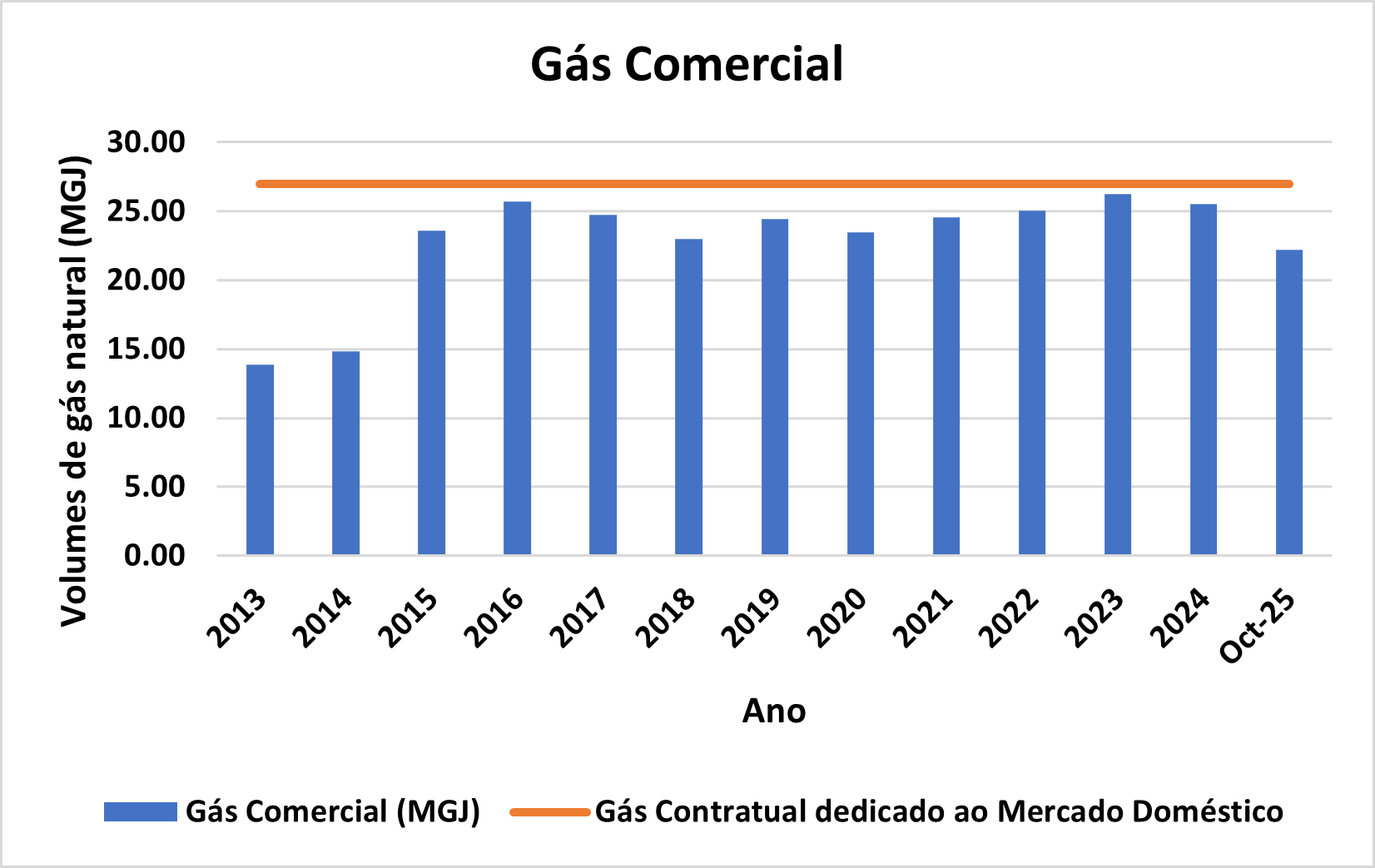

The APP in addition to the supply of gas to the South African market through GSA 1 & 2, also includes the provision of 27 MGJ/a to the national market through GSA3. This combined amount of IPP in kind (about 9 MGJ/a) is used on the national market for electricity generation, vehicle supply, homes and fuel in different industries, as described in the section on natural gas for the domestic market (2.3.6).

The Production Sharing Agreement (PSA) was concluded in October 2000 between the Government, ENH and Sasol Petroleum Mozambique Lda (SPM), with the objective of researching, evaluating, developing and producing non-associated natural gas and light oil from areas adjacent to the APP area.

Under contract, the Field Development Plan was approved in 2015 and in 2020 the respective amendment aimed at producing natural gas and light oil from the deposits of Inhassoro, Temane and Pande, to enable the construction of an Integrated Processing Infrastructure (IPF) with the following specifications :.

The infrastructure was commissioned and opened on 3 December, and production is expected to start in December 2025.

On 26 October 2000 the terms and conditions of the Mozambique-Sacunda Gas pipeline Agreement (Mozambique – Second Pipeline_MSP) were concluded between the Government (represented by the Ministry of Mining and Energy Resources), Sasol Limited (Sasol) and Mozambique Pipeline Investments Company Limited (ROMPCO), with the aim of transporting natural gas from Pande and Temane fields to supply the national and South African market.

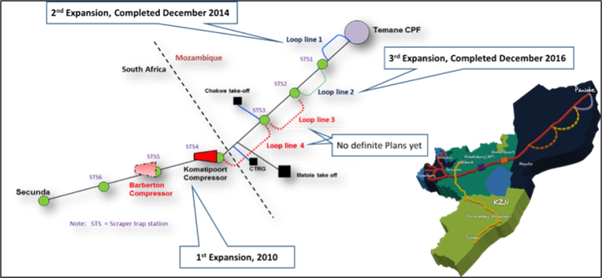

Under this contract and in accordance with the approved Gasoduct Development Plan, ROMPCO was granted the right to build and operate the 26-inch diameter pipeline, 867 km long and capable of transporting 122 MGJ/a.

With the increase in gas demand, the gas pipeline capacity was increased to 212 MGJ/a by installing a compressor on the South African side and two pipelines parallel to the main pipeline (Looplines) on the Mozambican side, as illustrated in the figure below.

Figure: MSP pipeline

The pipeline in question has 05 take points on the Mozambican side, which can be used as connecting points for the supply of natural gas in the southern region of the country.

Under the Gasoduct Grant Agreement signed in January 2003 between the Matola Gas Company (MGC), Gigajoule Africa Ltd, (GIGA) and the Government of the Republic of Mozambique, MGC has been granted the right to build and operate an 8-inch transmission pipeline and 70 km long, to transport natural gas from the Pande and Temane fields of the MSP pipeline take point in Ressano Garcia to Matola and to provide the various industries, services and housing in Maputo province.

Operated by MGC, the pipeline provides natural gas to the distribution network of Maputo and Marracuene and supplies gas to more than 30 companies including Maputo thermal power station.

Research and Production Grant Agreement (CCPP), for Area 4, in the Rovuma Basin was concluded between the Government and Eni East Africa, S.p.A. (EEA) and National Hydrocarbon Company, E.P (ENH), holding 90% and 10% respectively. Currently, the shareholder structure of Area 4 includes the Mozambique Rovuma Venture (MRV) SpA that is a Joint Venture co-ownership of Eni, ExxonMobil and CNODC, with 70% of participatory interest, National Hydrocarbon Company E.P. (ENH), with 10% of participatory interest, Galp Energy Rovuma B.V.. with 10% of participatory interest and KOGAS Mozambique Ltd..with 10% of participatory interest.

Area 4, located approximately 250 km northeast of the city of Pemba (Provincia de Cabo Delgado), 50 Km from the coast, measured from the western border of the concession, at depths of water ranging from 1,800 to 2,600 meters. The Area is about 70 km wide and 200 km long. To the west, a straight line border divides Area 4 of Area 1.

In order to maximize the production of the Coral Eocene 441 warehouse, the MRV, Area Operator 4 submitted the proposal of the Development Plan (PdD) of the Northern Coral Project FLNG consisting of the construction of a floating natural gas processing and liquefaction infrastructure (FLNG) for the production of 3.55 MTPA of liquefied natural gas, installation of wells and underwater production systems, storage and loading of LNG and condemned, which was approved by the Council of Ministers by Decree No 9/2025 of 11 April.

With the approval of this PD it is expected that they will be available for use in the domestic market up to 25% of the total oil and gas to be produced, and 10% will be available at the beginning of production, i.e. in the second half of 2028.

Following the approval of the PD of the Northern Coral Project FLNG, the Concessionary took on October 2, 2025, in Maputo, the Final Investment Decision that consolidated Mozambique as an Energy Power, positioning the country as the 14th largest exporter of LNG and the 4th in Africa. The project envisages an investment of around 7.2 billion dollars and start of production for 2028.

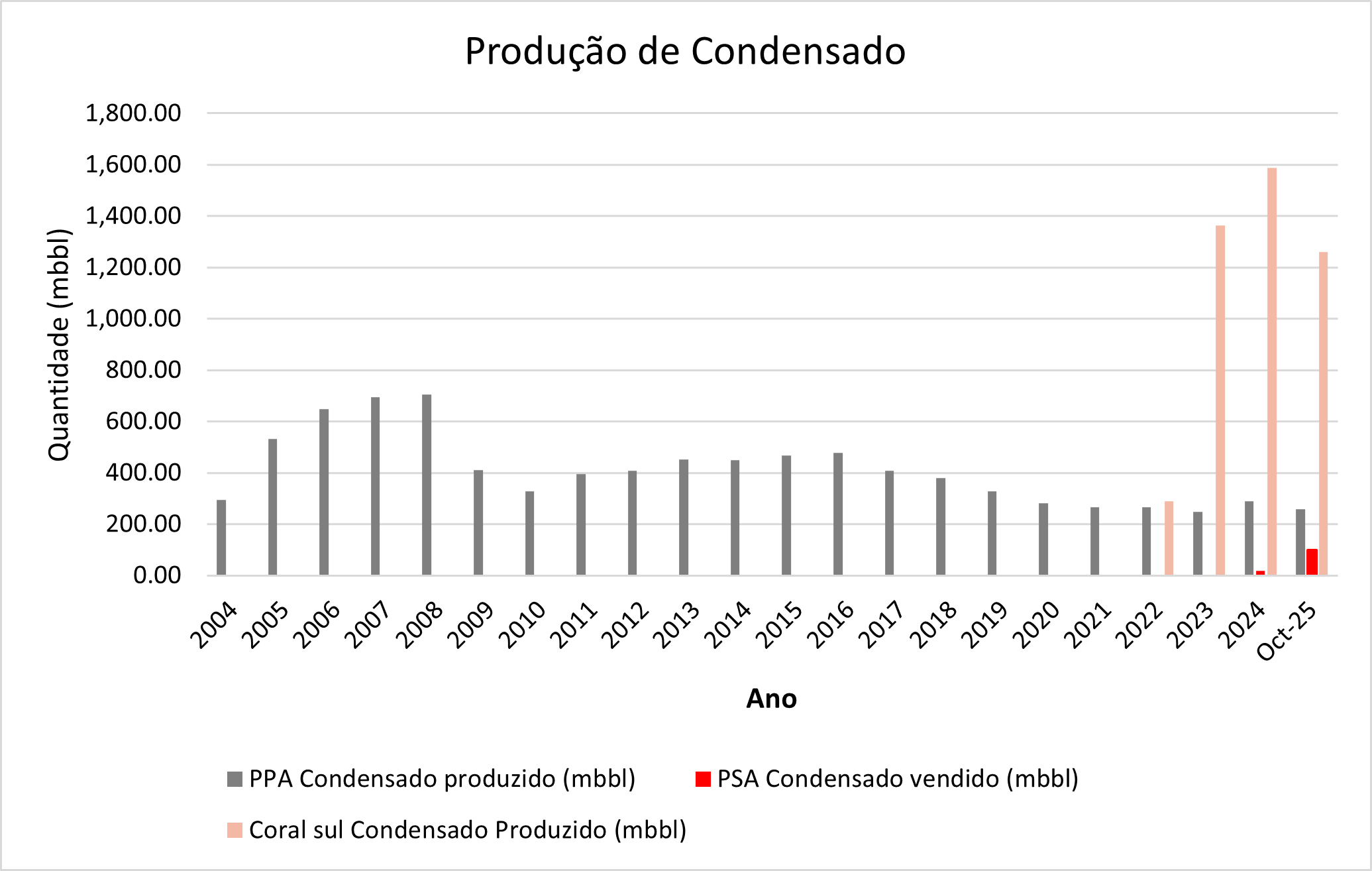

Under the CCPP, the Government approved the Southern Coral Project Development Plan FLNG, for the development of Coral Eocene 441, with the aim of producing and marketing natural gas through a natural gas Liquefaction Floating Unit, with the capacity to produce 3.37 MTPA (Million tonnes per year) of Liquefied Natural Gas (LNG) subsequently expanded to 3.55 MTPA. In addition to the LNG the condensate is produced and exported from this project.

The final Investment Decision for the implementation of the project was reached in 2017 and started the construction of the Southern Coral FLNG oil infrastructure in 2018,

In 2022, the Oil Infrastructure docked in Mozambican territorial waters and the anchoring process, inspections, inspections and certifications began in accordance with the applicable legislation that culminated in the issue of the operating licence in August 2022.

The production of LNG through the project began in October 2022 and in November of the same year the first shipment of LNG and Condensed dedicated to export was carried out.

On 26 December 2006 the terms of the Oil Research and Production Agreement were approved, "CCPP", to Area 1, Offshore of the Rovuma Basin, concluded between the Government, Anadarko Mozambique Area 1 Lda., as Dealer and Operator, (AMA 1 or Operator) and National Hydrocarbon Company, E.P. (ENH), with a participation of 85 and 15%, respectively. Currently, the participating interests in this Area 1 include TotalEnergies E&P Mozambique rea1, Lda. (TEPMA1) with 26.5%, Mitsui E&P Mozambique Area1 Limited (MEPMOZ) with 20%, the National Hydrocarbon Company, E.P. (ENH) with 15%, BPRL Ventures Mozambique B.V (BPRL) with 10%, Beas Rovuma Energy Mozambique Limited (BREML) with 10%, NGOC Videsh Rovuma Limited (ONGC Videsh) with 10% and PTTEP Mozambique Area1 Limited (PTTEP MZA1) with 8.5%.

Under the CCPP, the Government approved the Development Plan of the Golf Course/Atum, for the development of the Golf/Atum Project (Mozambique LNG) consisting of the production of Liquefied Natural Gas (LNG) through two Natural Gas Liquefaction Modules, with a capacity of 6.56 MTPA each, totaling 13.12 MTPA (Million Tons per Year). In addition to LNG production, the project provides for the provision of a total of 400 MMscfd for the domestic market, with 100 MMscfd being first provided.

In June 2019, the Operator announced the final investment decision (FID) for the implementation of the project.

In May 2021, Area 1 Operator declared the Force Major and consequent interruption of activities in Palma and Afungi. The force major was lifted to continue the project.

In addition to the deposit Coral Eocene 441, the Dealers of Area 4 intend to develop Campo Mamba, through the Rovuma LNG Project Development Plan, to be implemented on land. The same was approved by the Council of Ministers by Resolution No 29/2019 of 05 June. .

The Rovuma LNG Project consists of two Natural Gas Liquefaction Modules, with a capacity of 7,6 MTPA each, totaling 15,2 MTPA (Million tons per year), through the resources from the Mamba field located in Area 4 offshore From the Rovuma Basin.

The development of the activities related to this project has suffered a setback due to the instability and security situation in the north of Cabo Delgado Province, which led to the Area Operator 1 Offshore of the Rovuma Basin to activate the Force Major clause and consequent interruption of activities in Palma and Afungi, facilities shared by Area 1 and Area 4, forcing concessionaires to maintain the project in suspensive conditions.